Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

I understand renting can be a convenient and affordable option for many people. I say that as a person who helps people buy and sell homes every day. However, if you’re considering remaining in a particular area for a few years, it may be worth exploring your mortgage loan options. Owning a home provides you with the stability of a permanent residence. It can also serve as an investment that can appreciate over time, building your wealth.

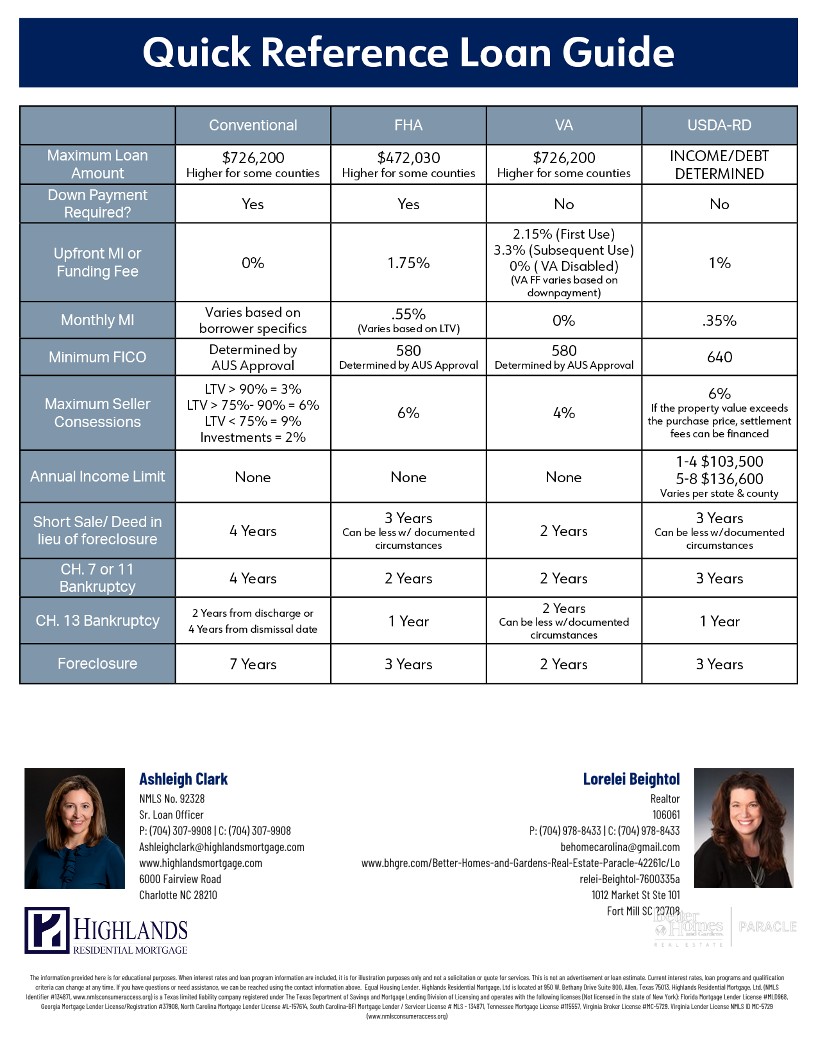

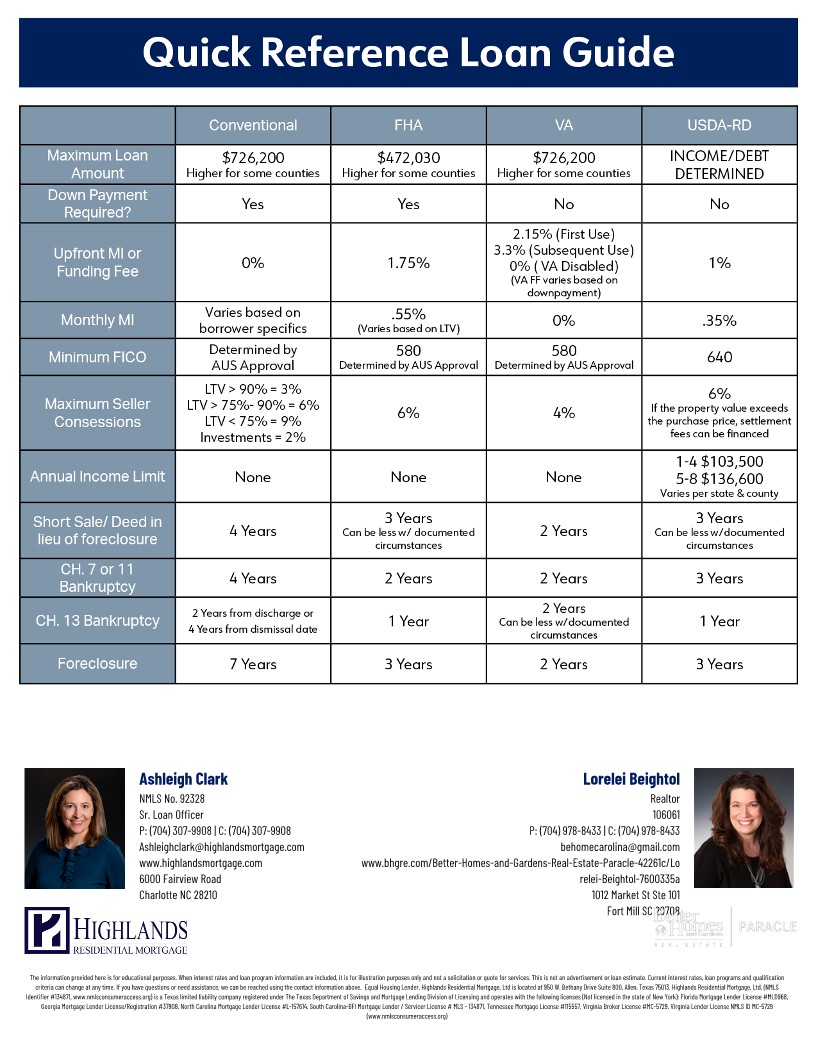

Your Options

Before you start your search for the perfect home, it’s essential to understand the different types of mortgages available to you. Here are a few options that you may want to consider:

- Fixed-Rate Mortgage: A fixed-rate mortgage is a popular option for many homebuyers. With this type of mortgage, the interest rate stays the same throughout the life of the loan, so your monthly payments remain consistent. This can make budgeting much easier and provide you with peace of mind knowing that your payments won’t increase.

- Adjustable-Rate Mortgage: An adjustable-rate mortgage (ARM) is a type of mortgage that starts with a fixed interest rate for a specific period, typically five or ten years, after which the interest rate adjusts annually based on the current market rate. While an ARM can initially offer lower interest rates, it’s important to understand that the rate can increase significantly after the initial fixed period.

- FHA Loan: A Federal Housing Administration (FHA) loan is a government-backed mortgage that is designed to help first-time homebuyers and those with lower credit scores. With an FHA loan, you can qualify for a down payment as low as 3.5%, making it an excellent option for those who don’t have a significant down payment saved up.

- VA Loan: A VA loan is a mortgage loan available to veterans and their families that are guaranteed by the Department of Veterans Affairs. With a VA loan, you can qualify for a down payment as low as 0%, making it an excellent option for those who have served in the military.

- Jumbo Loan: A jumbo loan is a mortgage that exceeds the conforming loan limits set by Fannie Mae and Freddie Mac. Jumbo loans are typically used for luxury properties and require a higher down payment and credit score.

Final Thought

When considering mortgage options, it’s important to evaluate your financial situation and determine how much you can afford to borrow. Speak with a mortgage lender to determine what options are available to you and what you qualify for. Talk to my friend Ashleigh at Highlands Mortgage if you are ready to explore your options.

Owning a home is a significant investment. It can provide long-term stability and financial benefits. Explore your mortgage options to find the right loan to fit your needs and budget. Once you know you qualify to buy, the fun begins with looking for your new home.

Mortgage Loan Options